Philippine real estate sector still resilient mid year despite ongoing headwinds Lobien

In this preferred, middle, more realistic scenario, the real estate sector should perform close to 2025 levels up to the end of 2026. “Hopefully, inflation will be managed, and the interest rates will slowly go down,” Lobien said.

Different markets

On the office front, the business process outsourcing (BPO) firms are projected to bring in 70,000 new employees in 2026 which in turn will require at least 300,000 sqms of space. These companies now account for 52 percent of total space leased, an increase from the 45 percent in the two earlier quarters.

The research showed the breakdown of the other industries that were looking for office space during the first quarter of 2026: traditional offices, 34 percent; government, 10 percent; and others, 4 percent.

“The BPO industry at 52 percent - they’re really the ones getting the available spaces out there,” said Lobien. “But due to hybrid work or work from home, they’re not growing at the levels like pre-pandemic.” The BPO industry has retained its lead as the occupier of the office market, although the government agencies — which Lobien said had the “budget, the money, and can afford to upgrade their old offices and facilities” — was a strong contender last year.

Meanwhile, the residential property market is still sensitive to the fluctuations of the economy, the state of mortgage rates, and inflation. One particular risk lies in the potential disruption of OFW remittances coming from the Middle East.

Still, market resilience can be seen in the increase in prices. The Metro Manila condominium prices in particular, have risen by 3.7 percent YoY and 13.2 percent QoQ. The overall total country price index also saw a growth of 4.5 percent YoY and 5.6 percent QoQ. The Balance Greater Manila Area (GMA), referring to CALABARZON, Central Luzon, and nearby provinces, has overtaken the NCR when it comes to residential loans granted (40 percent vs. 29 percent). Emerging infrastructure in the related areas, post-pandemic demand for bigger homes, and lower property prices have contributed to this development.

Lobien also pointed out a longstanding opportunity: the national housing backlog, which the Department of Human Settlements and Urban Development has estimated at 5.8 million homes. “The star here is the affordable and economic low-cost housing in the P2.5 million to P10 million range per unit,” she said. “That’s what many Filipinos can afford.”

Finally, the Philippine warehousing market, valued at $441.7 million in 2025, is estimated to grow at a 5.2 percent Compound Annual Growth Rate (CAGR) for the next eight years. Occupiers have been focusing on Batangas, Cavite, and Laguna. Lower land costs, international airport access, and connectivity through expressways have led to the rise of Clark and Central Luzon as the country’s fastest-growing logistics hubs.

As the report concluded, despite the global headwinds, Philippine “real estate - particularly office and industrial - is positioned to remain a relative bright spot through year-end.”

Source:

https://www.manilatimes.net/2026/07/15/business/real-estate-and-property/philippine-real-estate-sector-still-resilient-mid-year-despite-ongoing-headwinds-lobien/2384780/amp

">

Halfway through 2026, the Philippine real estate sector is still proving to be resilient despite the economic shocks brought by the Middle East crisis, as well as uncertainties brought about by the recent tumultuous movements in the Senate. The IT-BPM industry has increased its office market share in Metro Manila from 45 percent to 52 percent in the first quarter. The resilience of the residential property sector can be seen in the rise of its prices, with the total country price index growing 4.5 percent year-on-year (YOY). Finally, the continuous expansion of warehouse and logistics investments beyond the National Capital Region (NCR) is fueled by factors like infrastructure projects, e-commerce growth, and supply chain modernization.

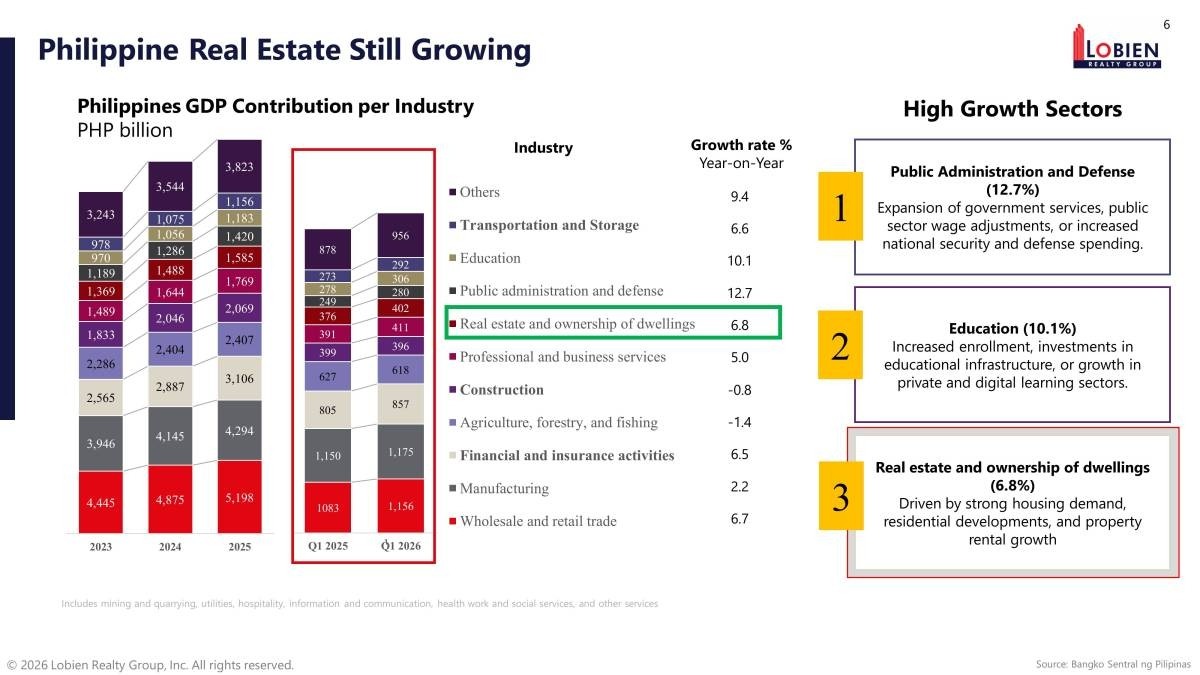

Lobien Realty Group (LRG) Founder and CEO Sheila Lobien further pointed out, “Real estate as a sector grew 6.8 percent year-on-year in the first quarter despite the headwinds — that’s one of the clearest signs that demand fundamentals remain intact.”

On July 9, Lobien shared her company’s findings during their mid-year media briefing, which discussed the future of the Philippine real estate sector, its emerging trends, investment performance, and emerging opportunities.

LRG is one of the Philippines’ fastest-growing commercial real estate consultancies, providing strategic advisory and transaction services across office, industrial, retail, investment, and project leasing. LRG combines deep market intelligence with global best practices to help occupiers, landlords, developers, and investors make informed real estate decisions.

The LRG research showed that real estate at 6.8 percent still ranks as the country’s third-highest-growth sector, following public administration and defense (12.7 percent) and education (10.1 percent). Trailing real estate are wholesale and retail trade (6.7 percent), transportation and storage (6.6 percent), and financial and insurance services (6.5 percent). Real estate’s growth in turn is attributed to “strong housing demand, residential developments, and property rental growth.”

With the global economy directly affecting the industry, LRG modeled three different scenarios of the Middle East crisis and its various impacts on the latter. It then assigned a 50 percent probability to a “fragile truce” base case, which Lobien described as a middle ground that is “not the best but still not the worst.” That situation would peg the country’s GDP from 3.5 percent to 4.1 percent; inflation from 4.5 percent to 5.5 percent; the Bangko Sentral ng Pilipinas policy rate at 4.75 to 5 percent; and the US dollar-Philippine peso conversion rate at P59 to P61. The remittances from the OFWs, a major market of developers, would stabilize as the Middle East region normalizes.

In this preferred, middle, more realistic scenario, the real estate sector should perform close to 2025 levels up to the end of 2026. “Hopefully, inflation will be managed, and the interest rates will slowly go down,” Lobien said.

Different markets

On the office front, the business process outsourcing (BPO) firms are projected to bring in 70,000 new employees in 2026 which in turn will require at least 300,000 sqms of space. These companies now account for 52 percent of total space leased, an increase from the 45 percent in the two earlier quarters.

The research showed the breakdown of the other industries that were looking for office space during the first quarter of 2026: traditional offices, 34 percent; government, 10 percent; and others, 4 percent.

“The BPO industry at 52 percent - they’re really the ones getting the available spaces out there,” said Lobien. “But due to hybrid work or work from home, they’re not growing at the levels like pre-pandemic.” The BPO industry has retained its lead as the occupier of the office market, although the government agencies — which Lobien said had the “budget, the money, and can afford to upgrade their old offices and facilities” — was a strong contender last year.

Meanwhile, the residential property market is still sensitive to the fluctuations of the economy, the state of mortgage rates, and inflation. One particular risk lies in the potential disruption of OFW remittances coming from the Middle East.

Still, market resilience can be seen in the increase in prices. The Metro Manila condominium prices in particular, have risen by 3.7 percent YoY and 13.2 percent QoQ. The overall total country price index also saw a growth of 4.5 percent YoY and 5.6 percent QoQ. The Balance Greater Manila Area (GMA), referring to CALABARZON, Central Luzon, and nearby provinces, has overtaken the NCR when it comes to residential loans granted (40 percent vs. 29 percent). Emerging infrastructure in the related areas, post-pandemic demand for bigger homes, and lower property prices have contributed to this development.

Lobien also pointed out a longstanding opportunity: the national housing backlog, which the Department of Human Settlements and Urban Development has estimated at 5.8 million homes. “The star here is the affordable and economic low-cost housing in the P2.5 million to P10 million range per unit,” she said. “That’s what many Filipinos can afford.”

Finally, the Philippine warehousing market, valued at $441.7 million in 2025, is estimated to grow at a 5.2 percent Compound Annual Growth Rate (CAGR) for the next eight years. Occupiers have been focusing on Batangas, Cavite, and Laguna. Lower land costs, international airport access, and connectivity through expressways have led to the rise of Clark and Central Luzon as the country’s fastest-growing logistics hubs.

As the report concluded, despite the global headwinds, Philippine “real estate - particularly office and industrial - is positioned to remain a relative bright spot through year-end.”

Source:

https://www.manilatimes.net/2026/07/15/business/real-estate-and-property/philippine-real-estate-sector-still-resilient-mid-year-despite-ongoing-headwinds-lobien/2384780/amp

Tags: real estate resilience